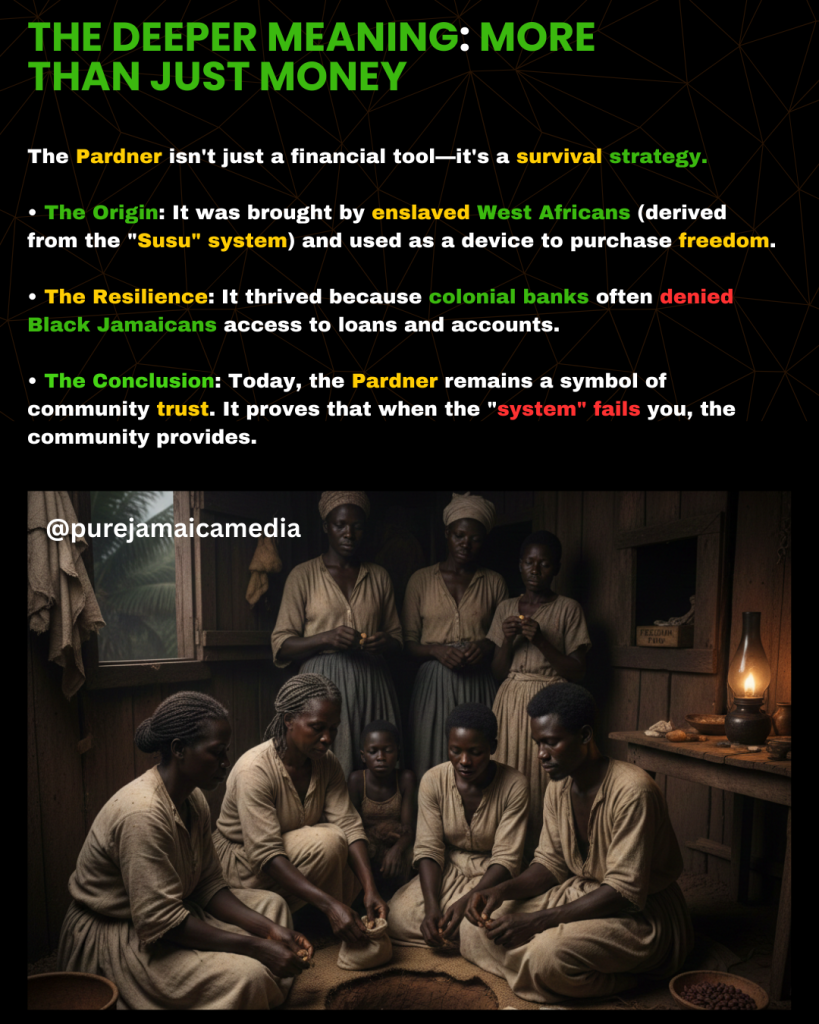

In Jamaica, while shiny bank towers and digital apps dominate the skyline, there is one financial institution that requires no paperwork, no credit score, and no monthly fees: the Pardner.

Rooted in centuries of African tradition and refined by the necessity of the Windrush generation, the “Pardner” system remains arguably the most culturally reliable and emotionally disciplined way for Jamaicans to save. It isn’t just a financial tool; it is a contract of trust.

How the Pardner System Works

The system is a form of Rotating Savings and Credit Association (ROSCA). It operates on a simple cycle of collective contribution and individual payout. Here is the anatomy of a Pardner:

1. The Key Players

• The Banker: The most critical role. This person must be beyond reproach. They organize the group, collect the money, and ensure the right person gets paid on time. In modern times, the Banker may take a small “cut” or the first “draw” as a management fee.

• The Pardners: The members of the group (friends, family, coworkers, or church members) who agree to contribute a fixed amount.

2. The Vocabulary

• The Hand: The fixed amount of money each person pays in every period (e.g., $5,000 JMD per week).

• The Draw: The total lump sum collected from everyone, which is given to one member at each interval.

• The Throw: The act of making your scheduled payment.

Real-World Examples

To understand why this beats a traditional savings account for many, let’s look at two scenarios:

Example A: The “Early Draw” (The Interest-Free Loan)

Imagine a group of 10 coworkers. Each agrees to “throw a hand” of $10,000 every week.

• Total Pot: $100,000 per week.

• Scenario: Member #1 needs to pay their child’s CXC exam fees immediately. They request the first draw.

• The Result: In Week 1, Member #1 receives $100,000. They have essentially received an interest-free loan that they will “repay” by continuing to throw their $10,000 hand for the next 9 weeks.

Example B: The “Late Draw” (The Disciplined Savings)

In the same group of 10, Member #10 wants to buy a new refrigerator but struggles to keep money in a bank account without spending it.

• Scenario: They request the last draw.

• The Result: For 10 weeks, they are forced to be disciplined because “the Banker is coming for the money.” In Week 10, they receive a lump sum of $100,000. For them, the Pardner acted as a high-discipline savings account with a guaranteed goal.

Why It Remains “Most Reliable”

While banks offer interest (which is often eaten up by fees), the Pardner offers social accountability.

1. Zero Barriers: No TRN, no utility bill, and no minimum balance are required—only your word.

2. Forced Discipline: You can ignore a banking app notification, but you cannot easily ignore a Banker standing at your door or desk. The “shame” of failing the group is a powerful motivator to save.

3. Community Wealth: It keeps money circulating within a trusted circle rather than sitting in a corporate vault.

The Modern Twist

Even in 2026, the system hasn’t died; it has evolved. While many still use “hard cash,” others now use bank transfers to the Banker or dedicated “Pardna Apps” that automate the collection and rotation while maintaining the traditional structure.